Vietnam has rapidly become one of ASEAN’s most attractive host countries for Foreign Direct Investment (FDI), but the era of measuring success by volume of investment alone is coming to an end. The real challenge for the country is improving the quality of foreign direct investment to foster sustainable, long-term growth. The goal of attracting […]

The outbreak of COVID-19 led to slower growth in consumer lending in Vietnam with consumers taking a more cautious approach to borrowing due to the uncertainty created by the pandemic. However, with the world transitioning into a new normal era, Vietnam’s economy started to bounce back swiftly. This resulted in the double-digit growth of consumer credit, specifically in terms of gross lending and outstanding balance with consumers seeing card lending as an optimal way to manage their finances.

Highlights of Vietnam’s Consumer Finance Market

Market size and growth

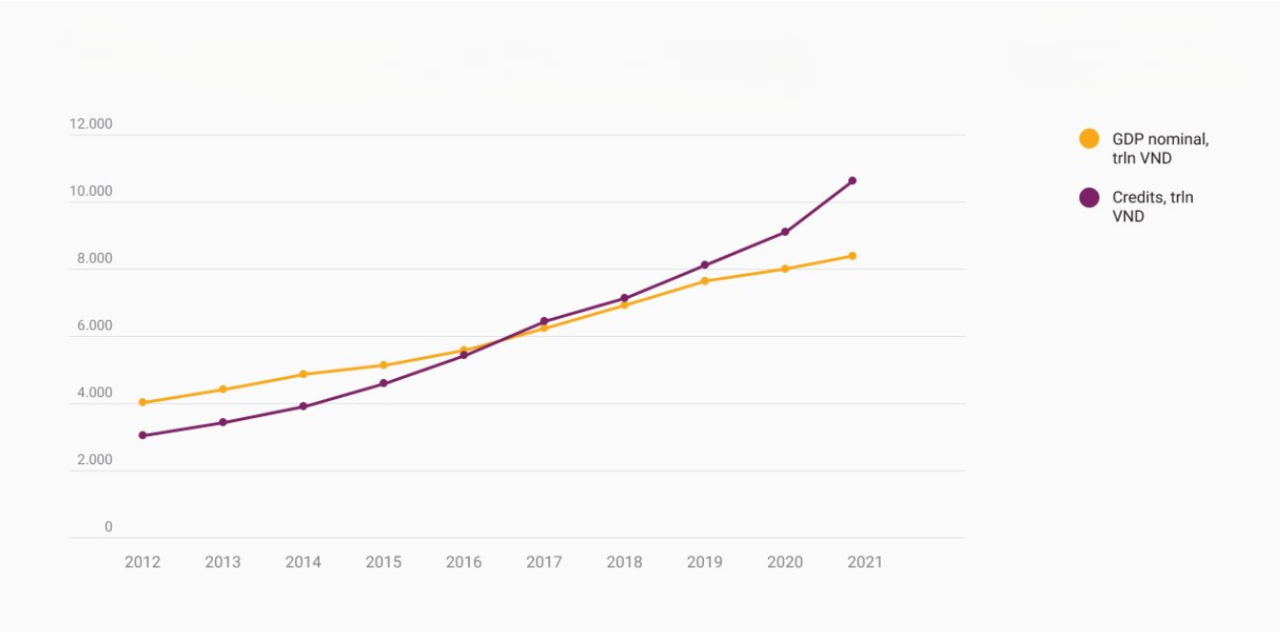

Twenty years ago, Vietnam’s consumer finance market barely existed. Since then, the explosion of e-commerce and a rapid-growing tech-savvy generation has set off an exponential growth in this sector. Between 2017 and 2021, the industry went through an unprecedented growth with a compound annual growth rate (CAGR) of 15.1%.

From January 2020 to July 2022, the country’s volume of loans soared compared to previous years, increasing by 39.5% to 5.6 trillion VND. Also, during the same period, the country’s GDP reported a significant improvement of 12.07%. Which means, according to the calculation of Robocash Group’s experts, for every 1% increase in lending volume, Vietnam’s GDP will increase by approximately 0.6%. Looking at the proven data, we see a strong correlation between the growth of Vietnam’s GDP and consumer loans value.

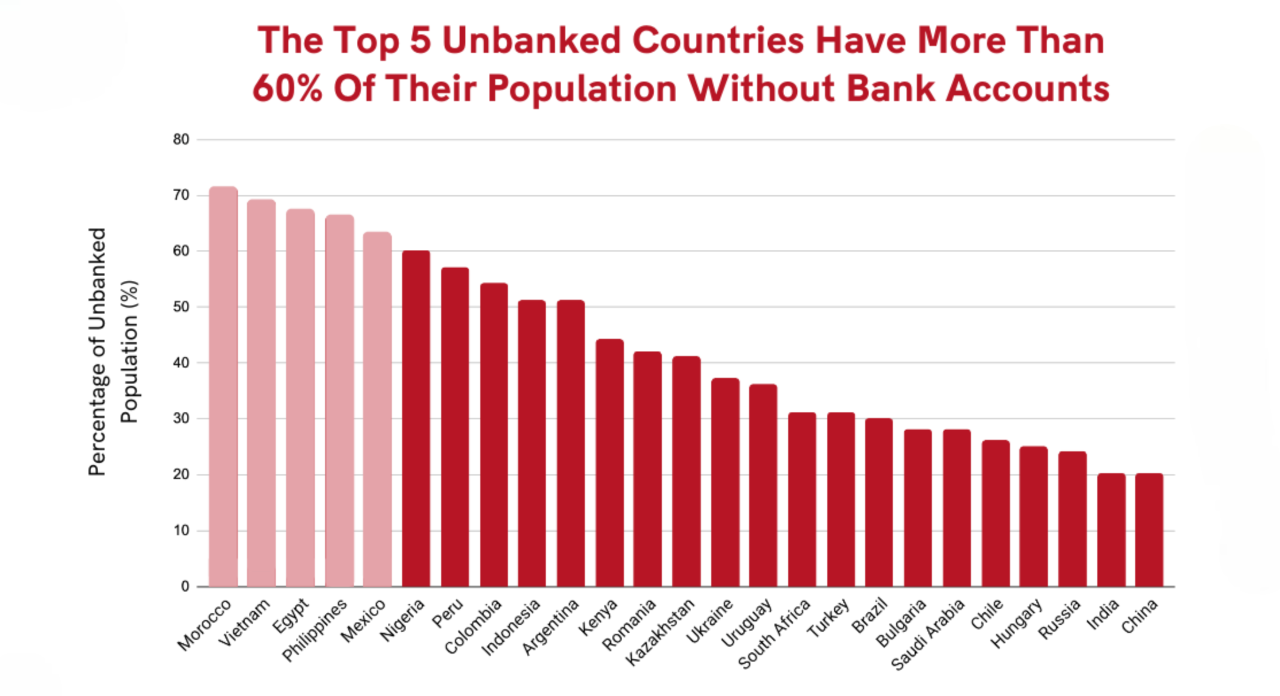

The importance of consumer finance to the broader Vietnamese economy cannot be overlooked, especially when nearly 70% of the country’s adult population is unbanked or underbanked. The Vietnamese government sees consumer finance companies, who are serving those unbanked or underbanked customers, as a critical positive force to help drive greater financial inclusion and accelerate economic growth.

Types of consumer finance products

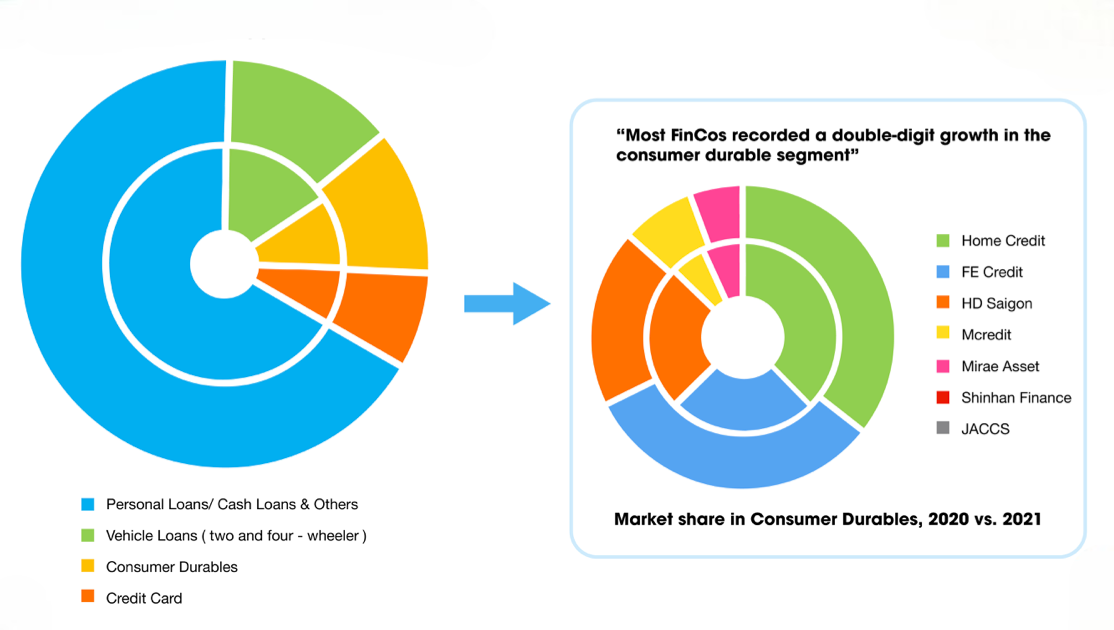

In terms of product offerings, cash loans, which refer to loans being directly disbursed to consumers’ accounts, still mount up to approximately 60% of the total portfolio. Consumer durables loans and vehicle loans experienced a downward trend in the past few years, whereas credit cards reported a double-digit growth. This coincides with other Fincos’ plans to boost credit card offerings as a cash loan alternative, following the direction of the State Bank of Vietnam (SBV).

Market share

At the moment, the Vietnamese CF market comprises a total of 16 Fincos, all licensed and regulated by the State Bank of Vietnam (SBV). However, over 80% of the market is shared by three main players: FE Credit, Home Credit, and Mcredit. The sector is also witnessing a sharp augmentation in foreign investors’ interest in this fast‐growing sector in Vietnam, through multiple M&A deals led by Japanese investors such as SMBC (JPN), Shinsei Bank (JPN), and Credit Saison (JPN).

Unpacking Vietnam’s Regulatory Environment for Consumer Finance Sector

Consumer finance as regulated in Vietnamese law

Consumer finance is generally regulated by Law on Credit Institutions No. 47/2010/QH12; Circular No. 39/2016/TT-NHNN prescribing lending transactions of credit institutions or foreign bank branches, or both, with customers; and Circular No. 43/2016/TT-NHNN, as amended in 2019, prescribing consumer lending by finance companies. The Law on Credit Institutions provides two types of credit institutions permitted to provide consumer lending:(1) Vietnam-based commercial banks, foreign bank branches, and foreign-invested banks; and (2) Vietnam-based finance companies. Both banks and finance companies must obtain an operating license from the SBV and an enterprise registration certificate from the Department of Planning and Investment. Finance companies are limited to providing loans not exceeding 100 million VND (except for car loans with security). Non-credit institutions such as fintech companies are currently not allowed to provide consumer lending.

Promoting Consumer Finance Amidst Concerns over Illegal Moneylenders

The Consumer Finance sector is expected to undergo significant changes in the coming years with some policy adjustments. Notably, Circular No. 17/2021/TT-NHNN on bank card operations officially established an official legal framework for card issuance using the electronic method, facilitating digital banking development as well as credit card adoption. Besides, the draft decree guiding mechanisms for fintech operation in the banking sector provides a full-fledged legal framework that encourages innovation, prevents financial risk, and promotes financial stability.

Also, in the first half of 2022, SBV continued the accommodative monetary policy it adopted in March 2020 to support businesses while monitoring new inflation trends. The State Bank maintained the refinancing interest rate at 4%, continued its guidance on loan forbearance, and encouraged commercial banks to waive or reduce interest rates and fees to assist businesses affected by the COVID-19 pandemic. These policies have helped maintain strong credit growth and ensure ample liquidity in the market. SBV is also monitoring the rise in inflation driven by the global commodity price shock, focusing on its management through closer coordination between monetary and fiscal policy, especially in the 2022-23 socio-economic support package.

Alleviate Challenges and Capitalizes on future Opportunities

Major Challenges

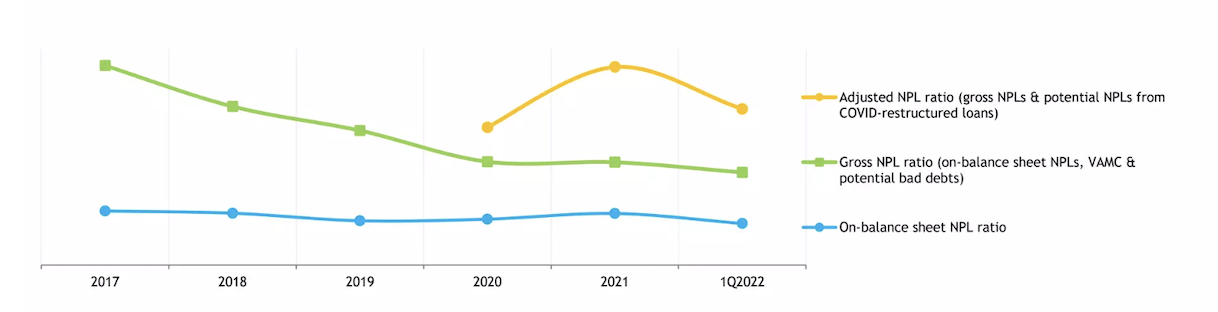

(1) Asset Quality Declination

First, it is difficult to increase the scale of consumer finance rapidly if asset quality is at risk of declining due to customers' vulnerability to the impact of Covid-19 pandemic, which has caused waves of job loss and income reduction.

Figure 5: Non-performing loan (NPL) ratios of credit institutions. Source: FiinGroup JSC

According to data collected as of June 2022, Vietnamese FinCos’ NPL ratios still remained at a high level. Going forward, the asset quality of FinCos is expected to improve in the coming time along with strong credit growth and recovered debt repayment capacity of borrowers. However, given such deterioration, it will take some quarters or even a year for FinCos' customer portfolio of subprime borrowers to recuperate to the pre-pandemic asset quality level.

(2) Fierce Competition

Up to this point, Vietnam’s consumer finance sector has still been in its early stages of development. Thus, it is inevitable that the number of startups and enterprises wishing to break into this playfield will burst in the next few years to come, which leads to even more fierce competition for market share and profits. Such a landscape can lead to a declination in lending interest rate in a race to win over potential customers. Meanwhile, financial companies still have to borrow capital from primarily credit institutions and the bond market with relatively high-interest rates.

Not to mention, with FE Credit, Home Credit and Mcredit accounts for over 80% of the whole market share, it has become more difficult than ever for new CF players to compete if they can show no distinct advantage over other competitors.

(3) Regulatory Constraints

Another challenge for the consumer lending market in Vietnam is that the legal framework is taking an increasingly rigorous and cautious stance, which can contribute to the improvement of the credit institution landscape, but at the same time, can negatively affect the scope of operations and profitability of financial companies.

What’s next for consumer lending in Vietnam?

Given the bumpy road ahead, the future of Vietnam’s consumer lending market remains promising due to a significant change in consumer’s consumption and borrowing habits. The combination of the country’s rapid economic recovery, rising per capita income, and the exponential growth of the middle class has ultimately sparked off an increase in demand for credit and consumer lending. Also, the fact that nearly 69% of the Vietnamese population is unbanked or underbanked is presenting ample opportunities for finance companies to jump in and capitalize on.

To add up, the strong digital transformation process has created many opportunities for the consumer lending market to modernize, diversify products, improve customer experience, reduce costs and increase consumer access.

With that being said, here are the 3 key trends and developments that will drive the market in the upcoming time.

(1) Buy now, pay later (BNPL) is poised to thrive as a new customer acquisition & retention channel

One of the key trends in the consumer finance market in Vietnam is the rise of the BNPL referred payment method. With over 64 million smartphone users in the country, BNPL is becoming an increasingly popular way for consumers to access credit. Companies like HomeCredit, Fundiin, Atome, and Litnow are leading the way in this space, offering quick and easy-to-access mobile-based loan products and payment services.

(2) Pawnshops' activities flourished posing fierce competition to mainstream CF providers

Besides consumer finance as unsecured loans, other collateral-based loans such as pawnshop business are also catching investors’ eyes.

According to Forbes data, as of June 2022, Vietnam has over 30,000 pawn shops, with more than 2,300 stores in Ho Chi Minh City and close to 1,700 in Hanoi. If each had lent about VND 1 billion ($43,000) on average, then the outstanding loans would hit a total of VND 30 trillion ($1.3 billion).

With a total of 830 stores across the country, F88 is currently the biggest pawn shop chain in Vietnam, followed by Vietnmoney, Camdonhanh, Dong Shop Sun, Happy Money, Ok Money, etc. In early March 2023, the company has reported to raise over $50 million of fresh funding from Mekong Capital and Vietnam-Oman Investment Funding.

(3) M&A may heat up again with potential targets

Dealmaking in the Consumer Finance sector is certainly heating up, fueled by buoyant foreign capital under both direct acquisition and indirect acquisition via regional parent entities. With increasingly fierce competition, M&A would be an optimal solution for CF companies to maintain a competitive position in the imminent years.

Final Thoughts

Given all the challenges ahead, the future of consumer finance remains bright. From new advances in technology to increasing domestic demand, the possibilities are endless for companies working in this rapidly changing industry. If businesses want to rapidly surpass competitors, expand networks and unlock their business potential, connecting with a third party so that the two can jointly support the development, search, and establishment of new business hubs must be a prudent option. Our comprehensive advisory service platform at Viettonkin enables a holistic approach to help both domestic and foreign investors address any legal or operational issues within the context of their own unique operations.

Harness the full potential of your business with Viettokin today!